if war bad... why stocks go up?

0 up · 0 down · 0 ratings

Channels and socials

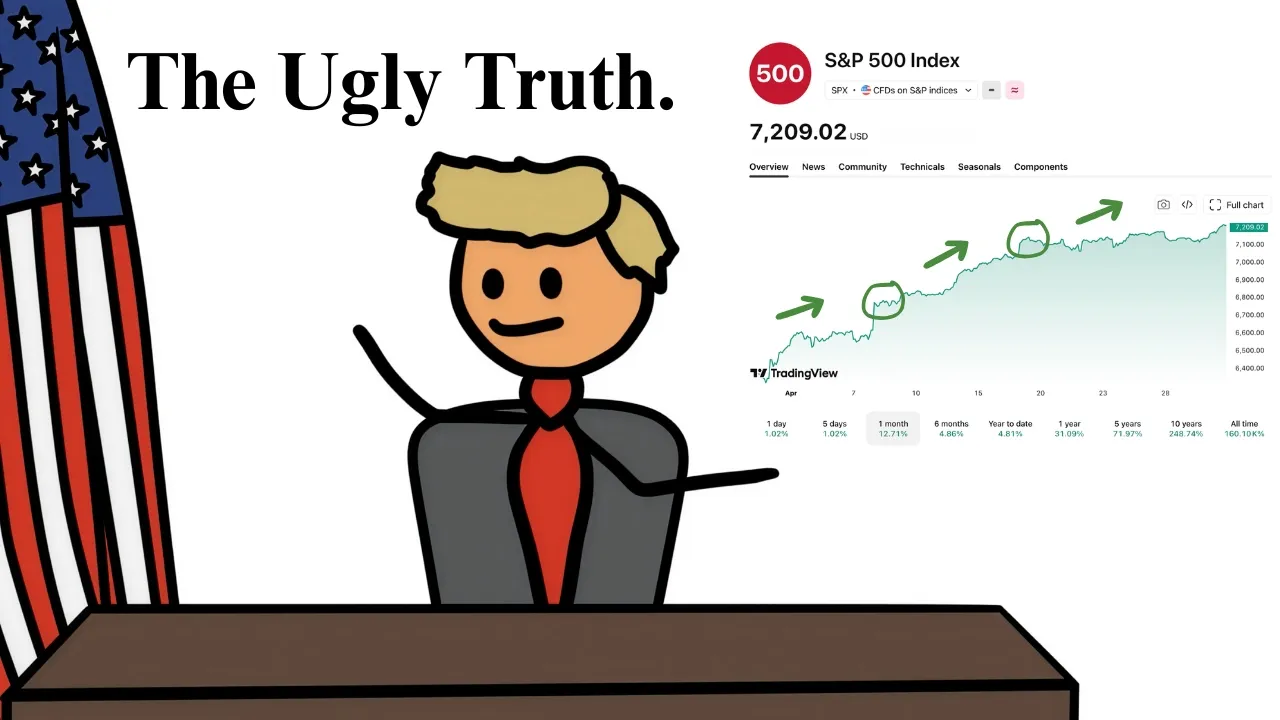

The biggest stock market rally of the year had nothing to do with peace, the news, or anything else you were told. Wall Street lied to you. On April 8th, the S&P ripped 2.5%, the Nasdaq jumped almost 3%, and the Dow had its best day in a year. Every financial outlet called it a "relief rally" on the back of the Iran ceasefire. But the truth is, this was not a relief rally. In this video, I'll break down: • Why hedge funds were selling at the fastest pace in 13 years • How a short squeeze actually works • The $86B of forced buying that compressed into five trading sessions • How commodity trading advisors and options dealers turned a squeeze into a full-blown melt-up • Why this exact pattern in the stock market keeps repeating Complex topics, simple breakdowns. Join my free weekly newsletter to stay ahead of what's actually happening in markets: casualmarkets.co All illustrations, visuals, and animations in this video are original and hand-drawn by a freelance artist. Disclaimer: The information provided in this video and on this channel (collectively, the “Content”) is for informational, educational, and entertainment purposes only and does not constitute investment, financial, legal, or tax advice, nor a recommendation to buy, sell, or hold any security or investment strategy. Investing involves risk and you must do your own research. Nothing in the Content should be interpreted as creating a fiduciary relationship, financial advisory relationship, or client relationship of any kind. The host, the channel, and all affiliated entities expressly disclaim any and all liability for any direct or consequential loss or damage arising directly or indirectly from the use of, reliance upon, or interpretation of the Content. By viewing or interacting with the Content, you acknowledge and agree to these terms and release the host and all related parties from any and all claims related to your reliance on the information provided. #economy #economics #wallstreet #stockmarket #investing #finance

On April 7, at 5:32pm, Donald Trump announced a ceasefire with Iran, and the next trading day markets quickly reacted to the reduced uncertainty. The S&P closed up 2.5%, the Nasdaq was up almost 3%, and the Dow climbed more than 1,300 points, its best day in almost a year. The video notes that traditional outlets described this as a “relief rally” tied to peace, but argues the ceasefire narrative does not explain why stocks stayed at record highs even as the ceasefire fell apart in real time. To explain the price action, the host rewinds to late February and March, including US and Israel airstrikes on Iran, Iran shutting down the Strait of Hormuz, and the resulting worst five-week losing streak in nearly four years for the S&P. The core setup is that, beneath the surface, Wall Street began to panic as hedge funds repositioned, selling at the fastest pace in 13 years, with leverage elevated. The host then describes the mechanics of the move, centering on a short squeeze rather than peace-driven fundamentals. Shorting is explained as borrowing shares, selling them, and later buying them back cheaper, with losses growing if the price rises. As price rises, margin calls force traders to add funds or close positions, and the resulting forced buying can push prices up further, creating the squeeze loop. On April 8, the video claims the squeeze began when macro short exposure was at the highest level since 2020, citing the idea that selling and short positioning had been extreme beforehand. The rally is framed as a sequence of “dominoes”: first the squeeze, then a systematic flip from commodity trading advisors that run rules-based models and flip from net short to net long, and finally options-dealer hedging described through a delta-neutral requirement and a negative gamma regime turning pro-cyclical. The host also highlights a specific quantitative claim, stating that forced buying totaled $86 billion across five trading sessions, far above an earlier estimate, which is presented as the driver of the melt-up. To close, the video argues that this pattern keeps repeating because the structure of the stock market has changed away from human-driven valuation work. It contrasts an older market where portfolio managers and analysts made discretionary decisions with today’s dominance of passive index investing, stating that about 63% of US stock funds are held by passive indexers. Because many passive funds are market-cap weighted, bigger companies receive more allocation automatically, and the “Magnificent Seven” is described as taking up over 33% of the S&P 500. The host adds that hedge funds are concentrated into large multi-strategy firms that often sell immediately when drawdown rules trigger, and that same-day expiration options are a major share of SPX trading. Options and dealer hedging are presented as real-time reaction engines, where large amounts of notional change hands and dealers hedge the underlying to stay balanced, stacking reactions on top of each other. The conclusion is that the headlines function as narratives to rationalize what happened, while the underlying driver is a feedback loop of automation, passive allocation, and options-dealer hedging that can make markets move “irrationally” for stretches of time.

Viewers generally praise the video’s clarity and entertainment value, often highlighting the mix of humor with detailed financial mechanics. A recurring theme is appreciation for the “irrational market” framing and the explanation of why stocks can rise during geopolitical stress, with many commenters echoing the idea that the stock market is not the same as the real economy. Some viewers report confusion or questions about the exact origin of the squeeze and the sequencing of forces, including who initiated it and how much movement came from short positioning versus other channels. Several comments raise a moral and systemic concern that wealthy actors and algorithmic trading can profit during conflict, with calls to regulate or even abolish the stock market and debate about banning high-frequency trading. There is also community interest in what comes next, including requests for predictions about a potential crash and how long the feedback loop could last, along with requests for clearer definitions of introduced terms.

Topics · finance · stock market · markets · economics · education · business

Questions answered

- How does a short squeeze work in stock markets?

- A short squeeze happens when short sellers are forced to buy back borrowed shares after the stock price rises. If enough traders receive margin calls at the same time, they must close short positions by buying shares, which pushes the price higher. The higher price can trigger additional margin calls, causing more forced buying and amplifying the move.

- Why can stocks rally on news of a ceasefire even when conflict is not resolved?

- The video’s explanation is that the rally can be driven by positioning and trading mechanics, such as existing macro short exposure, a short squeeze, systematic rebalancing by rule-based traders, and options-dealer hedging. These forces can create a self-reinforcing feedback loop where buying pressure increases price, which in turn triggers more hedging and more forced demand.

- What role do commodity trading advisors and rules-based models play in rapid stock buying?

- Commodity trading advisors are described as systematic firms that follow predefined trend-based rules rather than news. When their models flip from net short to net long based on price triggers, they can add large equity buying demand to cover or exit short exposure.

- How do options-dealer hedging and gamma regimes influence stock price momentum?

- When customers buy call options, dealers that must remain delta neutral may hedge by buying the underlying stock. In a negative gamma regime described as pro-cyclical, as the price rises dealers may buy more as a result of their hedging requirements, reinforcing upward momentum.